“One would have thought that it was even more necessary to limit population than property … The neglect of this subject, which in existing states is so common, is a never failing cause of poverty among the citizens; and poverty is the parent of both revolution and crime.”

(Aristotle, 384-322)

“The problem is that the population is growing the fastest where people are less able to deal with it. So it is in the very poorest places that you are to have a tripling in population in 2050.”

(Bill Gates, WEF, Davos, 2018)

“It would be extreme to regard China as uninvestable…no one could credibly claim Europe is uninvestable, just because of euro debt and banking crisis or Brexit.”

(Fred Hu, Primavera Capital Group, FT 2023)

“There is an enormous shift of power and influence in the world. It is mainly the story of China and India. It has never been in the past that powers emerge on such a massive scale without powers and revolutions. The challenge is how to maintain the peace in Asia in this century – it is not easy.”

(George Yoo Yong-Boon, Former Minister Foreign Affairs Singapore, WEF, Davos, 2008)

“There’s no doubt that the future belongs to Africa. Just think about it: by 2050, Africa will have the same population as China and India today, with rising consumer demand from a growing middle class. The cities will be booming, and the number of urban areas with populations of over 5 million people will rise. By 2050, Lagos, with a current population of about 18 million will double its size. The same would apply to Kinshasa, with a current population of 15 million. Three of the ten most populous nations will be African. Africa, which already counts about 230 million youths today (about 20 per cent of global youth population), will increasingly be the youngest continent.”

(Dr. Akinwumi Adesina, President of the African Development Bank, delivered by Vice-President Pierre Guislain at the Africa CEO Forum, Geneva, 2017)

“The world on which I was in government was a two power world. The world today is stronger, but there are intangible factors and the risks are more complex.”

(Henry Kissinger, Former US Secretary of State and National Security Advisor, WEF, Davos, 2008)

“The governments are victims of their own past, of their own prejudices. New organizations are unprecedented, they have no pasts, no prejudices, and have no border.”

(Shimon Peres, Former President of Israel, WEF, Davos, 2008)

“The crisis consists precisely of this: the old is dying and the new cannot be born: in this interregnum a great variety of morbid symptoms appear.”

(Antonio Gramsci, Notebooks, 1937)

It has become the narrative of the 21st century. The West as we have known it is losing its pre-eminent position. Emerging economies increasingly assume their larger role in the global economy. It is also clear that the emergence of these economies, including China, continues to be littered with obstacles.

The shift from the West to the East is accompanied by global insecurity, runaway global debt, protectionism, and conflict. The world is no longer controlled by the post-1945 allied western governments, but increasingly by bipolar centers of power. At the end of the current economic cycle that started in post-war 1945, the production of technology and consumer goods has been globally integrated across borders. Decoupling the 2 largest economies in the world would result in a dramatic and deep global economic recession. Janet Jellen, US Secretary of the Treasury, stated in recent interviews the US continues to have a very substantial trade and investment relationship with China, and emphasized US’ trade with China hit an all-time record in 2022, despite the political rift.

Figure 1. US-China Total Exports and Imports, 2000-2022. Source: US Commerce Department/Bloomberg, February 2023.

A large population, properly fed and educated, is a precondition to economic, political, and military power. Yet if population growth exceeds economic growth, if education, employment, and wages fall short of demand, population growth can lead to social unrest. Rapid population growth, urbanization, widening social inequality, industrialization, weak government and protectionism, have in history been precursors of domestic social conflict and trade wars, and ultimately, of war.

Since 1945 developed economies have benefited from large working-age populations that helped drive economic growth. But demographic hotspots are changing fast. It is difficult to believe that in 1950 Europe had twice as many inhabitants as Africa. Today Africa is projected to have 10 times the population of Europe by 2100. Japan, Western Europe, the United States, as well as China, are recording older and fast ageing populations, and accompanying lower productivity levels, with national GDP growth in these countries at lower levels compared to GDP growth in several emerging economies.

Argentina, Egypt, Ethiopia, Iran, Saudi Arabia, and the UAE have been invited to join BRICS in January 2024. It is one of many signals that the top emerging economies are securing a stronger representation on the geopolitical agenda.

Demographic Divide

Emerging economies in Sub-Saharan Africa and South Asia will account for almost all global population growth during the next 20 years. 50 Per cent of that growth will be concentrated in 9 countries: India, Nigeria, the Democratic Republic of Congo, Pakistan, Tanzania, the United States, Uganda, and Indonesia, outside the traditional economies of the Transatlantic economies, Japan, and Australia.

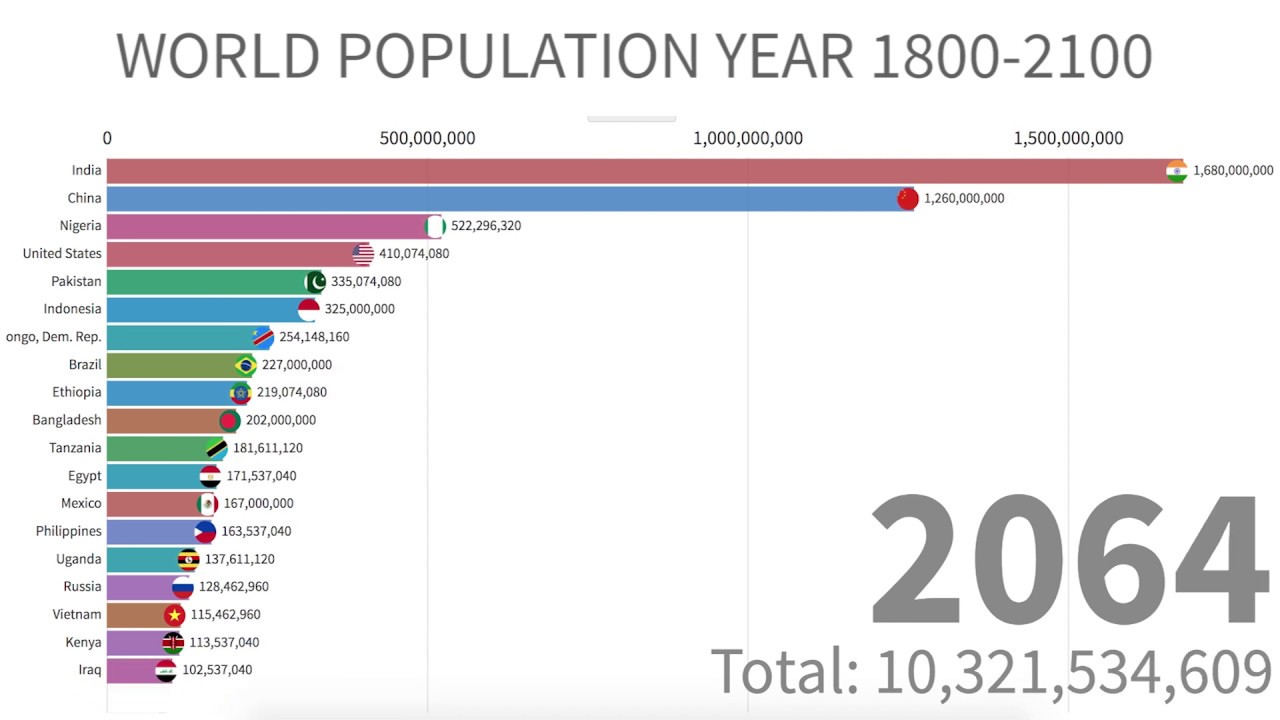

The current global population of 7.6bn is projected to reach 10.3bn in 2064, after which the population is expected to decline to 8.8bn by 2100, assuming fertility levels will continue to decline. India and China will remain the 2 most populous countries. Among the 10 largest countries worldwide, Nigeria is growing the most rapidly. The population of Nigeria, currently the world’s 7th largest, is projected to surpass the United States to become the 3rd largest country in the world close to 2050.

Unabated population growth puts unsustainable pressure on natural resource use and is likely to overwhelm countries’ capacity to provide the required infrastructure. The Lancet in 2020 published research data predicting population growth is unlikely to continue on a runaway upward trajectory. Instead, it is projected to naturally peak and decline due to global fertility rates after 2064. Given the astounding increase in populations in Africa and Asia already on the way, the pressure on resources, infrastructure, climate and education will however remain.

Figure 2. World Population in 2064, countries ranked according to population size. Source: Forbes (2020); Stein Emil Vollset cs, Fertility, Mortality, Migration, and Population Scenarios for 195 Countries and Territories from 2017 to 2100, The Lancet, July 2020.

The research data published in The Lancet indicate that 23, mostly developed, countries and China will see their population cut in half by 2100. Japan’s population has been projected to have peaked in 2017 at 128m, falling to 53m by 2100. China’s population is expected to peak in 2024 at 1.4bn, falling to 732m in 2100. Spain’s population is projected to have peaked in 2019 at 43m and is expected to fall to 22m by 2100. More and more countries today have fertility rates below the level required for the replacement of successive generations, which stands at roughly 2.1 births per woman. During 2010 to 2015, fertility was below the replacement rate in 83 countries comprising 46 per cent of the global population. The 10 most populous countries in this group are China, the Russian Federation, Japan, Vietnam, Germany, Iran, Thailand, and the United Kingdom (in order of population size).

Urbanization

A modern map of the world’s most populous cities in 2010 shows metropoles such as New York, Moscow, and Rio de Janeiro. Practically every continent could claim at least one of the most populous cities.

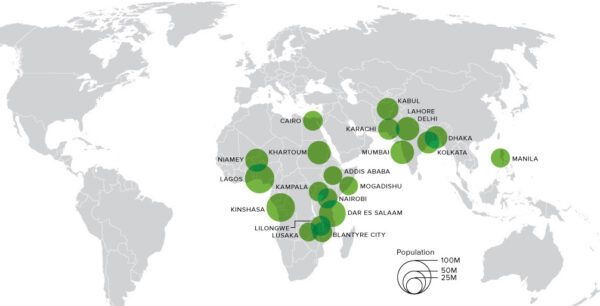

Figure 3a and 3b. Top-20 Cities Ranked By Population in 2010 and 2100. Source: Global Cities Institute/visualcapitalist.com, 2023.

Not any longer. Of the 20 largest cities in the world, with the exception of New York, in 2023 none of the cities with more than 20m inhabitants are located in the Americas, Europe, China, or Australia.

Figure 3b shows Lagos, with a population of 10.6m in 2010, is expected to have 88.3m inhabitants by 2100, an increase of 736 per cent. Kinshasa, the capital of the Democratic Republic of Congo, has already passed Paris as the largest French speaking city in the world. By 2100, Kinshasa has been projected to be the world’s second largest cities overall, with a population of 83.5m, an increase of 822 per cent (compared to 9.1m in 2010), with 60 per cent of Kinshasa’s population younger than 18 years. Next is Dar Es Salaam, a Tanzanian megacity that will hold 73.7m inhabitants in 2100 (compared to 4.4.m in 2010, a population explosion of 1,588 per cent. And then there are cities such as Blantyre City and Lilongure, of which I doubt many readers will have heard. In Sub-Saharan Africa, the median age will rise to 22 years by 2040, with more than one-third of Sub-Saharan’s population younger than 15 years in 2040, compared to only 14 per cent of the population in East Asia.

Emerging Economic Epicenters – Per Capita Poverty Lingers On

The complex correlation between demographic transition, industrialization, and economic growth that has swept the world since the late 19th century, is beyond the scope of this Bulletin. We project for the top-10 emerging economies to evolve as new economic epicenters, with 7 of the 10 largest global economies by GDP (PPP) in 2030 based in emerging countries.

Figure 4. Top 10 Countries by GDP (PPP) in 2030. Source: visualcapitalist.com, 2022.

Despite the impressive growth in GDP in emerging economies, relative per capita will take longer to grow. The top-10 emerging economies will not improve their relative per capita ranking among the traditional G-7 countries any time soon. Their average income in 2050 will still be 40 per cent below that of G-7 countries in 2023.

Emerging Stock Markets Overtake the United States

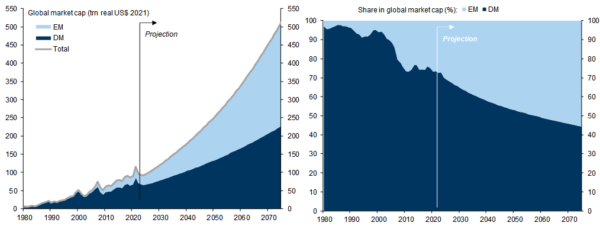

The stock market capitalization of emerging economies are projected to overtake the US and other developed economies in 2030. Although we see significant more capital flows in Shanghai and Shengzhen, this is in our view the long march, rather than a short term goal. Beijing’s regulatory policies wiped out $1tn of market value from Chinese equities since their peak in mid-February 2023. Another $3.2tn of market capitalization could be under threat, about a 6th of the market cap of Chinese listed companies. In September 2023, investors in an offshore bond issued by the world’s most indebted property developer Evergrande, were waiting for interest payments that had fallen due in previous days. With China facing the end of the country’s property-driven growth model, the Chinese government will have to find new growth drivers, to prevent the country from succumbing to long-term lower growth levels. The jury is still out.

Ray Dalio recently commented that China is not seeking a return to Maoism, but wants to correct a period when capitalism raised living standards but also create a large wealth gap and unsustainable high debt levels. According to Goldman Sachs Research, the emerging economies’ share of the global equity market will increase from 27 per cent in 2023 to 35 per cent in 2030, 47 per cent in 2050, and to 55 per cent in 2075. India is expected to have the largest increase in global market cap share, from under 3 per cent in 2022 to 8 per cent in 2050. China is projected to rise to 10 per cent – 15 per cent in 2050 but, due to a demographic and economic growth decrease, is projected to decline to 13 per cent in 2075. The US share of global equity markets is expected to fall from 42 per cent in 2022 to 35 per cent in 2030, to 27 per cent in 2050, and 22 percent in 2075. Japan and the Euro area are projected to decline, whereas Canada and Australia appear to show stronger growth potential in the decades ahead.

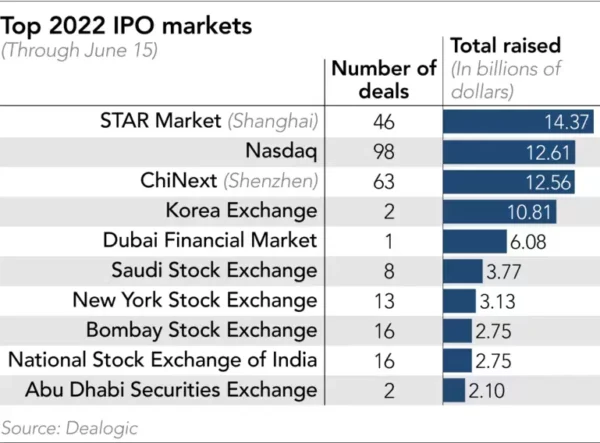

The main drivers are the equitization of corporate assets, the deepening of capital markets, new issuances and privatizations in emerging economies. In 2022 Shanghai Stock Exchange and Shenzhen Stock Exchange were, according to Deloitte China, set to retain 1st and 2nd positions in the global IPO ranking by funds raised as of 30 September 2022. Korea Stock Exchange came third, with Hong Kong and DIFC Dubai ranking at 4th and 5th place.

By the end of Q3/2022, the Chinese Mainland IPO market was projected to have 285 new listings raising RMB464.1b, a 23 per cent drop in the number of new listings compared to 2021, but a 26 per cent increase in raised capital, up from RMB 369,8b. During the same period, Hong Kong recorded 47 listings raising HKD54.7b, down from 73 IPOs raising HK288.5b in the same period in 2021.

Most emerging economies’ stock exchanges still do not have the liquidity to rival their counterparts in developed economies. Larger corporates in emerging economies need to tap into deep pools of capital as long as large pools of investors are not available in their domestic markets.

Shift in Global Governance

The ending of the decades-old correlation between the size of a national economy and per capita income shall have a profound impact on global geopolitical governance.

After nearly a century as the world’s preeminent superpower, the US will relinquish this title to China after 2030. The size of the US economy and its relative strong annual growth, combined with China’s deeply troubled domestic economy, will prevent China from rapidly outpacing the US, which will remain a global power. Relative per capita wealth in emerging economies will remain low. By 2050, the 5 largest economies, in both real $ US and PPP terms, will include 3 of the G-20’s poorest members: India, China, and Brazil. To compare: in 2010, 7 of the G-20 largest 8 members were among its richest in $ US terms. Average income in the G-20’s 10 emerging economies will rise in 2050 to $22,000, less than 60 per cent of the average income of the G-7 countries today. When calculated in PPP terms, the average income in emerging economies will be less than 50 per cent of the G7-countries’ income in 2050.

As a consequence, the traditional correlation between wealth and the size of a national economy in real $ US, will disappear, and will run negative in 2050 in PPP terms. As low- and middle income emerging economies increase their global market share, traditional distinctions between “developed” and “emerging”, and between “creditor nations” and “debtor nations”, wordings reminiscent of the colonial era, will become outdated.

The above will dramatically affect the role of supranational organizations and financial institutions. Although it is difficult, if not impossible, to forecast, how governments of these new economic epicenters will transform their economic growth into global governance, it is reasonable to anticipate that existing representative governance structures will no longer represent these fast growing markets, and are therefore likely to be marginalized over time.

@ Brun Lubert Corporation – All Rights Reserved

DISCLAIMER: The information and material presented herein are provided for information purposes only and should under no circumstance be U. S. ed or construed as a solicitation or offering to acquire, dispose, or engage in any financial dealing, including but not limited to the buying or subscribing for securities, investment products, or other financial instruments, nor to constitute any advise or recommendation with respect to such securities, investment products, or other financial instruments. This Bulletin is prepared for general circulation and has no regard to any class of investor or the specific investment objectives or particular needs of any specific person which may receive this Bulletin. Readers should independently evaluate the information and material contained herein before making any investment or other decision, and should take appropriate independent financial advice before making any investments or entering into any transaction in relation to any content mentioned in this Bulletin. It is a violation of U. S. federal and international copyright laws to reproduce all or part of this publication by email, facsimile or any other means. This document is not for attribution in any publication, and you should not disseminate, distribute, or copy this Bulletin, either in whole or in part, without the prior written consent of Brun Lubert Corporation.

Publisher – BRUN LUBERT CORPORATION

Enquiries – BRUN LUBERT CORPORATION

667 Madison Avenue

New York NY 10065

United States